Intraday mean reversion

Bounce

Buy the tick off the bottom, cap loss with a stop, trail the recovery, and review every fill.

price pathtrail active

Screen quant ideas. Backtest what survives.

A single-user strategy lab for turning filters into Bounce or Gravity systems, then testing them with assumption-aware fills before risking a dollar.

3,430

stocks

13F

signals

Paper

only

paper / backtest only

No live execution promises. No hidden optimistic assumptions.

Built for traders who distrust pretty equity curves.

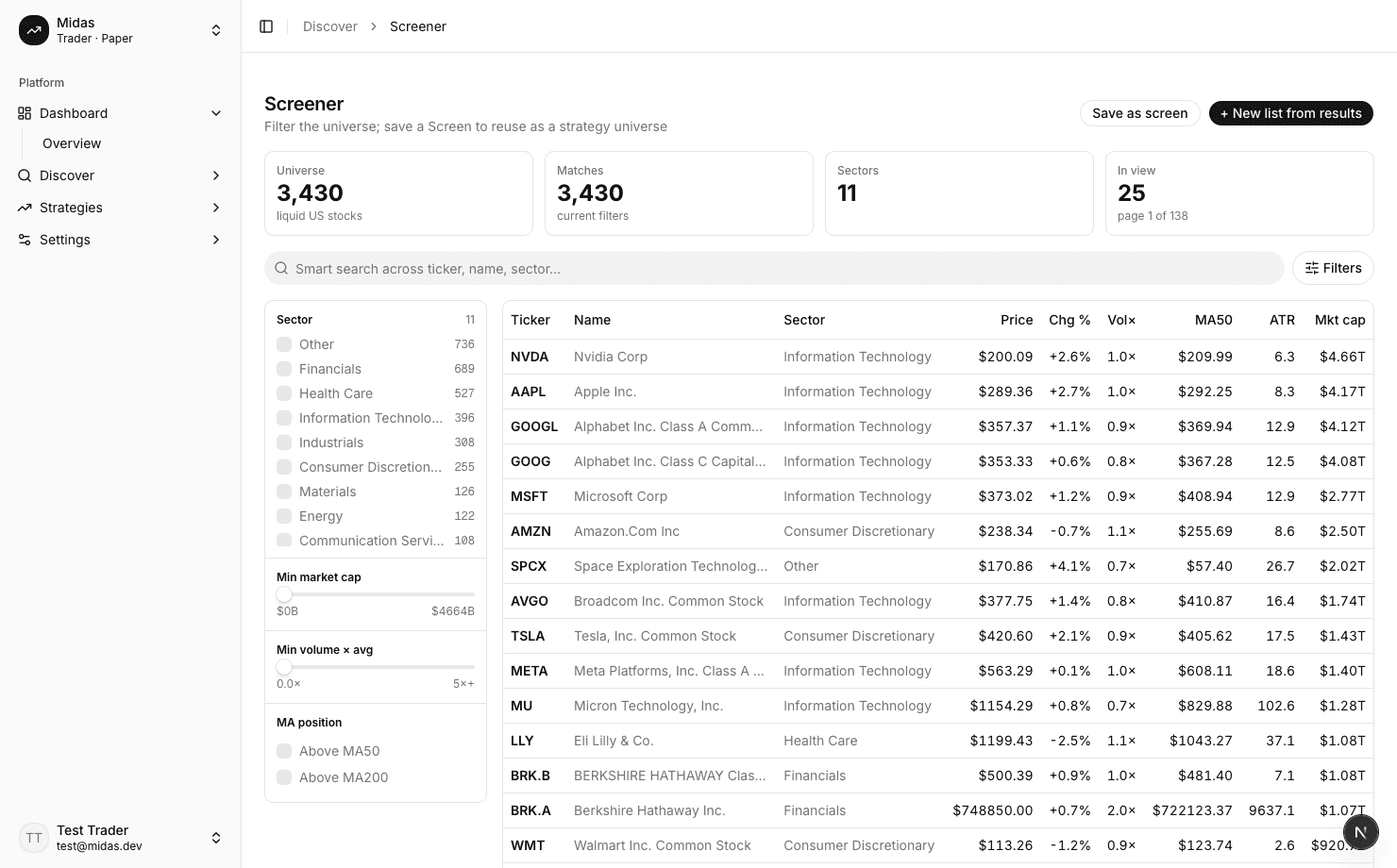

Screen by sector, volume, market cap, moving averages, and list membership. Save the result as a strategy universe.

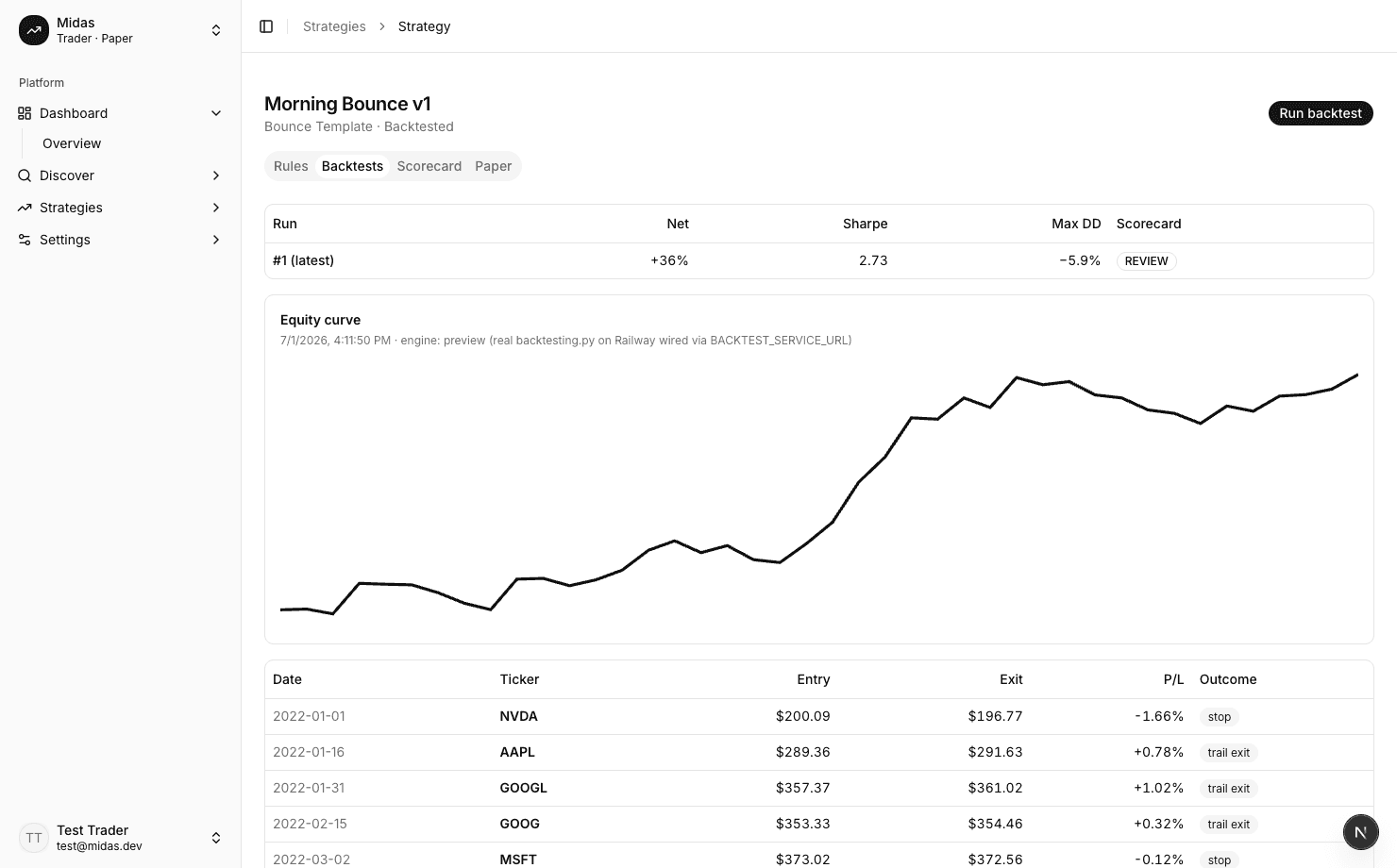

Morning Bounce v1

rules tab

Universe

Saved screen: liquid US names

Entry

Drop greater than 6%, first recovery tick

Exit

Trailing stop follows the bounce

Risk

Initial stop 1.05% below entry

Bounce is not a black box. Entry, exit, risk, universe, and trailing-stop behavior all sit in the open before the run begins.

Every result resolves into dates, tickers, entries, exits, P/L, and outcome tags. Pretty curves do not get to hide the trades.

Trades

auditable ledger

| Date | Ticker | Entry | Exit | P/L | Outcome |

|---|---|---|---|---|---|

| 2026-06-18 | AVGO | $1,734.20 | $1,759.80 | +1.48% | trail exit |

| 2026-06-18 | CRWD | $389.10 | $384.95 | -1.07% | stop |

| 2026-06-17 | NVDA | $142.80 | $146.32 | +2.46% | trail exit |

| 2026-06-17 | TSLA | $327.40 | $324.02 | -1.03% | stop |

Midas keeps the work inside one surface: screen the universe, define the rules, backtest honestly, then watch the strategy in paper mode.

Filter liquid US names by list, sector, volume, volatility, and moving averages.

Turn a saved screen into a Bounce or Gravity strategy with explicit entry, exit, and risk.

Model commission, slippage, intrabar stops, and filing-date-aware signals before you trust it.

Track passing strategies in a paper account view. Live execution stays gated.

Gravity timeline

signal to universe

13F filed

No look-ahead signal enters the test.

CIK resolved

Recorded before simulation.

Holdings dated

Recorded before simulation.

Screen saved

Recorded before simulation.

Backtest queued

Recorded before simulation.

The page is calm because the product is skeptical. Every attractive curve needs assumptions, dated signals, drawdowns, and a reason to survive out of sample.

Optimistic fills

Commission, slippage, and intrabar stop behavior are modeled by default.

Cherry-picked curves

Losers, drawdowns, trades, and assumptions stay visible in the review surface.

Look-ahead signals

13F and X inputs become dated signals before they enter a backtest.

Black-box verdicts

The scorecard shows why a strategy passed, warned, or failed.

Bounce watches sharp intraday overreactions. Gravity turns public signal sources into a dated, backtestable universe.

Buy the tick off the bottom, cap loss with a stop, trail the recovery, and review every fill.

Resolve a fund, date the holdings, fold in tracked accounts, and test the resulting pressure.

Connect the providers that power the loop. Broker surfaces are paper/connect UI only in v1.

source

Polygon

source

financialdatasets.ai

source

SEC EDGAR

source

twitterapi.io

source

Alpaca paper

source

Robinhood UI

Midas is deliberately narrow in v1: one user, honest testing, paper monitoring, no live order execution.

Open Midas, build a screen, and make the strategy prove itself before it earns your attention.